When a marriage or civil partnership comes to an end, the emotional weight is often compounded by one massive, looming question: “Who gets what?”

It is a common misconception in England and Wales that everything is simply sliced down the middle. You might have heard friends talk about a “50/50 split,” but the reality of UK law is far more nuanced. At Judge Law, we see firsthand how every family’s financial footprint is unique. The court’s primary objective isn’t mathematical equality, it is fairness.

Understanding how the courts approach financial settlements can help you move from a place of uncertainty to a position of strength. Whether you are worried about keeping the family home or ensuring your pension is protected, this guide breaks down the legal framework of divorce settlements in the UK.

The Starting Point: Fairness, Not Formulas

In England and Wales, there is no rigid formula for dividing assets. Instead, the legal system relies on the principles of fairness established in Section 25 of the Matrimonial Causes Act 1973.

While a 50/50 split of “matrimonial assets” (wealth built during the marriage) is often the starting point for the court’s deliberations, the final outcome is frequently different. The judge will look at the specific needs of both parties and, most importantly, the welfare of any children involved.

In practice, a settlement usually involves:

- Matrimonial Assets: Assets built up during the marriage are generally shared.

- The Family Home: This may be transferred to one spouse, sold, or held until a later date.

- Pensions: Accumulated pension wealth is often one of the largest assets and can be split or “offset.”

- Savings and Investments: These are pooled and divided based on future needs.

- Debts: These are factored into the overall “pot” to ensure the final division is realistic.

Further information about the formal legal process can be found on GOV.UK¹.

How Divorce Financial Settlements Are Decided

When a couple cannot agree on how to split their wealth, the court steps in. The judge uses a specific set of criteria to decide what a “fair” outcome looks like. This isn’t about “winning” or “losing”; it’s about ensuring both parties can move forward with financial stability.

The Section 25 Factors

The court considers several key elements:

- The Welfare of Children: This is the court’s “paramount consideration.” Ensuring children have a roof over their heads and their needs met comes before everything else.

- Income and Earning Capacity: What can each person earn now and in the future? If one spouse stayed home to raise children, their earning capacity might be lower, which the court will acknowledge.

- Financial Needs and Obligations: The court looks at what each person needs to live a reasonable life post-divorce.

- Standard of Living: The goal is to try, where possible, to maintain a standard of living similar to what was enjoyed during the marriage.

- Age and Length of Marriage: A 25-year marriage is treated very differently from a 2-year marriage.

- Contributions: This includes financial contributions (the breadwinner) and non-financial contributions (homemaking and childcare). In the eyes of the law, these are equal.

Typical Division of Assets in Divorce Settlements

To give you an idea of how different assets are handled, we have outlined the common treatments in the table below:

| Asset Type | How It Is Usually Treated | Possible Outcome |

|---|---|---|

| Family Home | Matrimonial property | Transfer to one spouse, sale and division, or deferred sale (Mesher Order). |

| Savings & Investments | Matrimonial assets | Divided fairly based on future needs and contributions. |

| Pensions | Part of financial resources | Pension sharing order, attachment order, or offsetting against the house. |

| Business Interests | Requires valuation | One spouse keeps the business while the other receives a larger share of other assets. |

| Debts | Shared or Individual | Liabilities are deducted from the total asset pool before division. |

Key Factors That Influence the Split

Because every family is different, settlements are rarely identical. However, the weighting of certain factors is predictable.

Housing needs carry significant weight. If there isn’t enough money for both parties to buy a new home, the court will prioritise the parent with whom the children will live most of the time. This might mean the other spouse receives less of the equity now in exchange for a “clean break” later.

Who Gets the House?

For most couples, the family home is the most valuable asset. The court has several tools at its disposal to deal with it:

- Property Transfer: Ownership is moved entirely to one spouse.

- Sale and Division: The house is sold, and the money is split (though not always 50/50).

- Mesher Order (Deferred Sale): The house stays in joint names, but one spouse lives there until a “trigger event” (like the youngest child turning 18). Then the house is sold and the proceeds split.

- Offsetting: One spouse keeps the house, and the other keeps the pension or a larger share of the savings.

If you are located in the Thames Valley and need local expertise on property values and legalities, our solicitors in Windsor or Maidenhead can provide tailored advice.

Pensions: The “Forgotten” Asset

Pensions are frequently overlooked, yet they can be worth more than the family home. In long marriages, the court views a pension built up during the union as a joint asset.

There are three main ways to handle this:

- Pension Sharing Order: A percentage of one person’s pension is transferred into a new pension for the other spouse.

- Pension Offsetting: You “buy out” your spouse’s interest in your pension by giving them a larger share of another asset (like the house).

- Pension Attachment Order: A portion of the pension is paid to the former spouse when the pension holder starts drawing it.

For complex pension queries, we recommend checking resources like the Pension Advisory Service² for general guidance.

Responsibility for Debts After Divorce

It is a common fear that you will be saddled with your ex-partner’s credit card debt. Legally, if a debt is in one person’s name, they are responsible to the lender. However, the divorce court looks at the purpose of the debt. If a loan was taken out for a family holiday or home improvements, the court may treat it as a “matrimonial debt” and reduce that person’s share of the assets accordingly to account for the repayment.

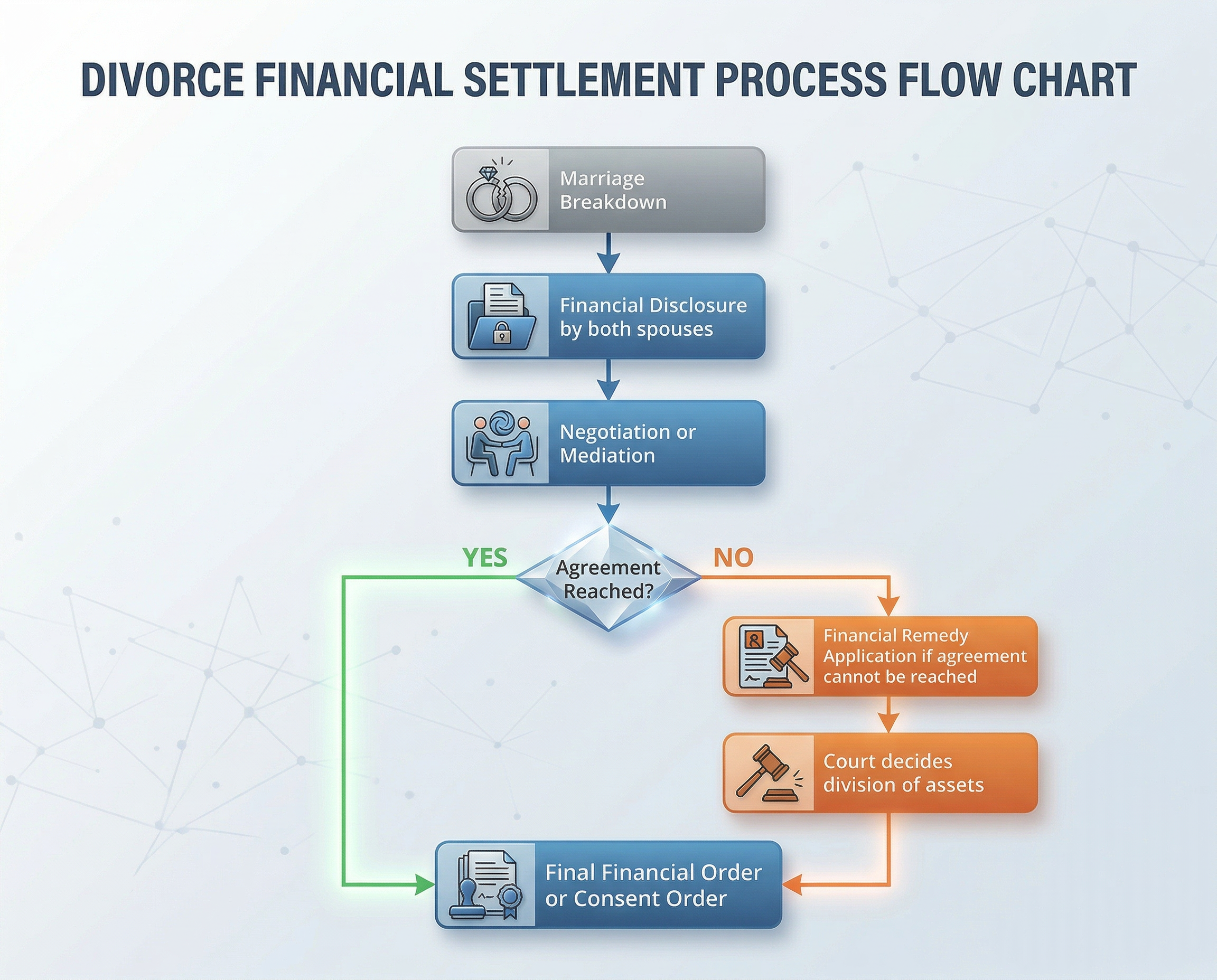

The Divorce Settlement Process

How do you actually get from “separating” to a “Final Order”? The path usually follows these steps:

- Financial Disclosure: Both parties fill out a “Form E,” detailing every penny they own and owe.

- Negotiation/Mediation: Using the disclosure, you try to reach an agreement. Mediation is often a mandatory first step unless there are safety concerns. (See the Family Mediation Council³).

- Consent Order: If you agree, a solicitor drafts a Consent Order, which a judge signs to make it legally binding.

- Financial Remedy Application: If you cannot agree, you ask the court to decide. This involves several hearings (FDA, FDR, and a Final Hearing).

When You Should Seek Legal Advice

While “DIY” divorces are possible for very simple cases, seeking legal advice is crucial if your situation involves:

- High-value property or multiple homes.

- Business interests or self-employment.

- Significant pension pots.

- International assets.

- A spouse who is being “economical with the truth” regarding their finances.

At Judge Law, we offer expert guidance across our offices, including Slough, Reading, and Guildford. We are here to ensure your settlement is not just “finished,” but truly fair.

Get Advice That Reflects Your Situation

Every divorce settlement is a puzzle with many moving parts. Understanding your potential entitlements early can prevent costly mistakes and provide the peace of mind you need to start your next chapter.

If you are ready to discuss your options with a reassuring, expert team, we are here to help.

Call us to speak to a member of the team immediately:

01753 331 095

Frequently Asked Questions

Does everything get split 50/50 in divorce?

No. While 50/50 is often the starting point, the court adjusts this based on “needs” and “fairness.” In many cases, particularly where children are involved, the split may be 60/40 or even 70/30.

Who gets the house if it’s in my name?

Legal ownership (whose name is on the deed) matters less in a divorce than you might think. If the property was the “matrimonial home,” the court has the power to award a share to the other spouse regardless of whose name is on the paperwork.

What happens to savings during divorce?

Savings accumulated during the marriage are usually treated as matrimonial assets and divided. Inheritances or savings brought into the marriage might be protected, but only if they haven’t been “mingled” with joint finances and aren’t needed to meet the other spouse’s basic needs.

Do I need a solicitor for a divorce settlement?

A solicitor ensures that your settlement is legally binding. Without a “Consent Order,” your ex-spouse could potentially make a claim against your finances (including future windfalls or lottery wins) many years after the divorce is finalised.

References:

¹ https://www.gov.uk/divorce

² https://www.moneyhelper.org.uk/en/pensions-and-retirement/pensions-and-divorce

³ https://www.familymediationcouncil.org.uk