Here's the uncomfortable truth: most people wait until they're sitting in a consultant's office, freshly diagnosed with early-stage dementia or recovering from a stroke, before they think about a Lasting Power of Attorney. By then, for many, it's already too late.

It's not your fault. We're hardwired to put off difficult conversations about our own decline. But in 2026, with an ageing population and increasing awareness of cognitive health, understanding the importance of Lasting Power of Attorney in the UK has never been more critical. This isn't about being morbid: it's about staying in control.

The Mental Capacity Cliff-Edge

Let's start with the legal reality. To create a valid Lasting Power of Attorney (LPA), you must have something called "mental capacity." Under the Mental Capacity Act 2005, this means you need to:

- Understand the information relevant to the decision

- Retain that information long enough to make the decision

- Weigh up the information to make a choice

- Communicate your decision

Sounds straightforward, right? The problem is that mental capacity isn't a gentle slope: it's often a cliff. One day you're making sound decisions, and the next, a medical event changes everything. A stroke at 3 AM. A fall that leads to delirium. The gradual fog of dementia that creeps in faster than anyone expected.

Once your capacity is lost, even temporarily, you cannot legally sign an LPA. It doesn't matter if you're having a "good day" or if your family knows exactly what you would have wanted. The law is absolute on this point.

This is what we call the Diagnosis Trap. The moment you most need an LPA in place: when your health is failing: is precisely when you lose the legal ability to create one.

What Happens Without an LPA?

If you lose mental capacity without an LPA in place, your family doesn't automatically gain the right to manage your affairs. Not your spouse. Not your children. No one.

Instead, someone (usually a family member) must apply to the Court of Protection to become your "deputy." This is the UK equivalent of guardianship, and it's a process you want to avoid if possible.

Here's why deputyship is the expensive, stressful alternative no one wants:

Time: The application process typically takes 6-9 months. During this time, bills pile up, care decisions hang in limbo, and your family is stuck in legal purgatory.

Cost: Application fees start at £371 for a property and affairs deputy, plus £385 for health and welfare. Then there are solicitor fees (often £2,000-£5,000), assessment fees, and ongoing supervision fees charged by the Court of Protection annually.

Restrictions: Unlike an attorney under an LPA, a court-appointed deputy has limitations. They may need court approval for major decisions, can't make gifts (even for inheritance tax planning), and are subject to ongoing supervision.

Emotional Toll: Imagine trying to navigate complex court forms, medical assessments, and legal proceedings while simultaneously caring for a loved one who's seriously ill. It's brutal.

The Financial Fallout

Beyond the immediate costs of deputyship, not having an LPA in place can wreak havoc on your estate planning strategy.

Consider this scenario: You own a property in Windsor that's increased significantly in value. Without an LPA, your family cannot make strategic decisions about that asset. They can't:

- Sell the property to fund your care

- Transfer ownership to a trust for inheritance tax purposes

- Access equity release schemes

- Manage rental income

Meanwhile, care home fees in the South East can easily hit £1,500-£2,000 per week. Without access to your assets or the ability to plan efficiently, families often drain savings unnecessarily or sell assets at the worst possible time.

A properly drafted Power of Attorney can include specific provisions for Inheritance Tax planning, giving your attorney the power to make gifts, create trusts, and implement tax-efficient strategies: all things a court-appointed deputy generally cannot do without jumping through additional legal hoops.

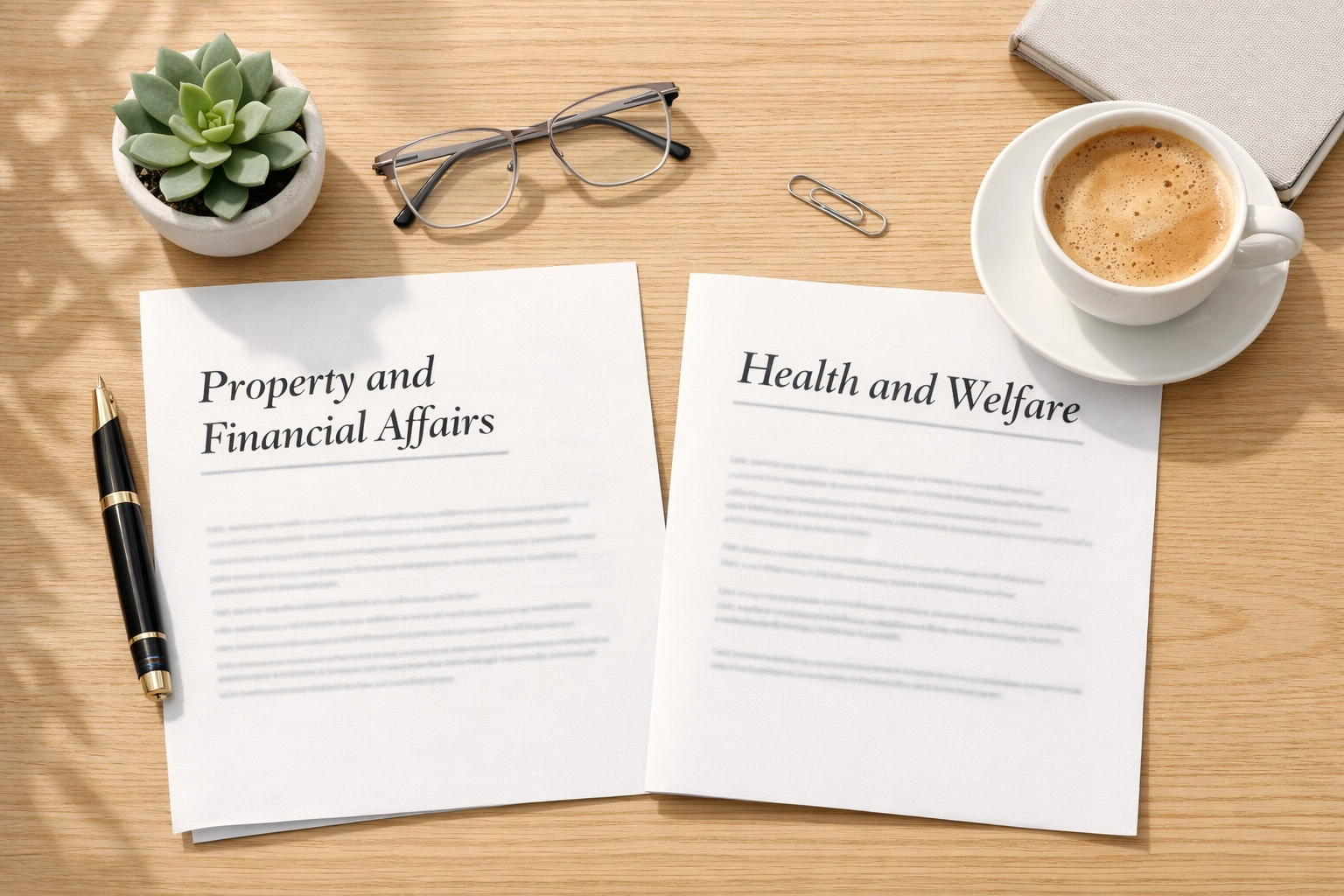

The Two Types of LPA (And Why You Need Both)

Since 2007, LPAs in England and Wales come in two flavours:

1. Property and Financial Affairs LPA

This covers decisions about your money and property, including:

- Managing bank accounts

- Paying bills

- Selling your home

- Managing investments

- Claiming benefits on your behalf

Crucially, this type of LPA can be used as soon as it's registered, even while you still have capacity. Many people use this for convenience (having a trusted attorney help with finances), long before any health issues arise.

2. Health and Welfare LPA

This covers decisions about your care and medical treatment, including:

- Where you live

- Your daily care routine

- Medical treatment decisions

- Life-sustaining treatment (if you've given explicit consent)

Unlike the financial LPA, this type can only be used once you've lost mental capacity. But when that moment comes, it's invaluable: allowing your chosen attorney to make decisions about care homes, medical procedures, and end-of-life care according to your wishes.

Most people need both. Together, they form a comprehensive safety net for your future.

When Is the Right Time? (Spoiler: It's Now)

If you're reading this and thinking, "I'm only in my 50s, I'll sort this out later," consider these statistics:

- 1 in 14 people over 65 in the UK have dementia

- 1 in 6 people over 80 have dementia

- Strokes can happen at any age, with 38% occurring in people under 65

But here's the thing: age isn't the determining factor. We've seen LPAs become essential for people in their 40s after unexpected medical events. Brain injuries from accidents. Early-onset dementia. Sudden strokes.

The right time to set up an LPA is when you have capacity: full stop. Waiting for a "warning sign" is playing Russian roulette with your family's future.

The Capacity Assessment Grey Area

Here's where things get tricky. Mental capacity isn't always black and white. Someone with early-stage dementia might have "good days" and "bad days." A solicitor must assess whether you have capacity at the moment you sign the LPA.

This creates a narrow window of opportunity. If you wait until symptoms are obvious, a solicitor may not be comfortable certifying your capacity. If the LPA is challenged later (which can happen), questions about capacity at the time of signing can invalidate the entire document.

The safest approach? Create your LPA while you're unquestionably well. Remove any doubt. Protect your future self from legal challenges that could tie up your affairs for years.

What About Updating an Existing LPA?

If you created an Enduring Power of Attorney (EPA) before October 2007, it's still valid: but only for property and financial decisions. You won't have the health and welfare protection that modern LPAs provide.

Similarly, if your circumstances have changed significantly since creating your LPA (divorce, remarriage, relationship breakdown with your chosen attorney), you need to create a new one. You can't simply amend an existing LPA: you must revoke it and start fresh.

This is where professional advice becomes essential. Our Wills and Estate Planning team can review your existing arrangements and identify any gaps that need addressing.

Taking Action: The Next Steps

Setting up an LPA isn't complicated, but it does require careful thought:

-

Choose your attorneys wisely. These should be people you trust implicitly: often family members, but sometimes close friends or professional attorneys.

-

Decide on decision-making. Will your attorneys act jointly (all must agree), jointly and severally (any can act alone), or a hybrid approach?

-

Include clear instructions. While not required, guidance about your preferences can be invaluable for your attorneys.

-

Register with the Office of the Public Guardian. An LPA isn't valid until it's registered, which takes 8-10 weeks on average.

The cost is relatively modest: £82 per LPA (or free if you're on certain benefits). Solicitor fees for drafting typically range from £200-£500 per LPA, depending on complexity.

Compare that to the thousands you'll spend on deputyship applications, and the decision becomes obvious.

The Bottom Line

The importance of a Lasting Power of Attorney in the UK in 2026 cannot be overstated. It's not about being pessimistic about your future: it's about being realistic. None of us know when we might need this protection, and by the time we do, it's often too late to act.

Don't fall into the Diagnosis Trap. Don't wait for the warning signs. Don't assume you have time.

If you haven't already set up your LPAs, or if you need to review and update existing arrangements, get in touch with our specialist team. We'll guide you through the process with the reassurance and expertise you need to protect yourself and your family.

Because the best time to set up an LPA is always the same: before you need it.