When people think about trusts, they often imagine a dusty old document locked in a safe, something that stays exactly the same for a hundred years. But in reality, a trust is a living legal relationship. It has a beginning, a middle, and an end: much like a business or even a person’s career.

At Judge Law, we often tell our clients that understanding the trust lifecycle is the best way to ensure their assets are protected without getting caught in legal spiderwebs. Whether you are setting one up for your kids or you’re a beneficiary wondering when you’ll actually see the money, knowing the milestones matters.

In this guide, we’re going to walk through the “birth” of a trust, how it’s managed (and changed), and how it eventually wraps up.

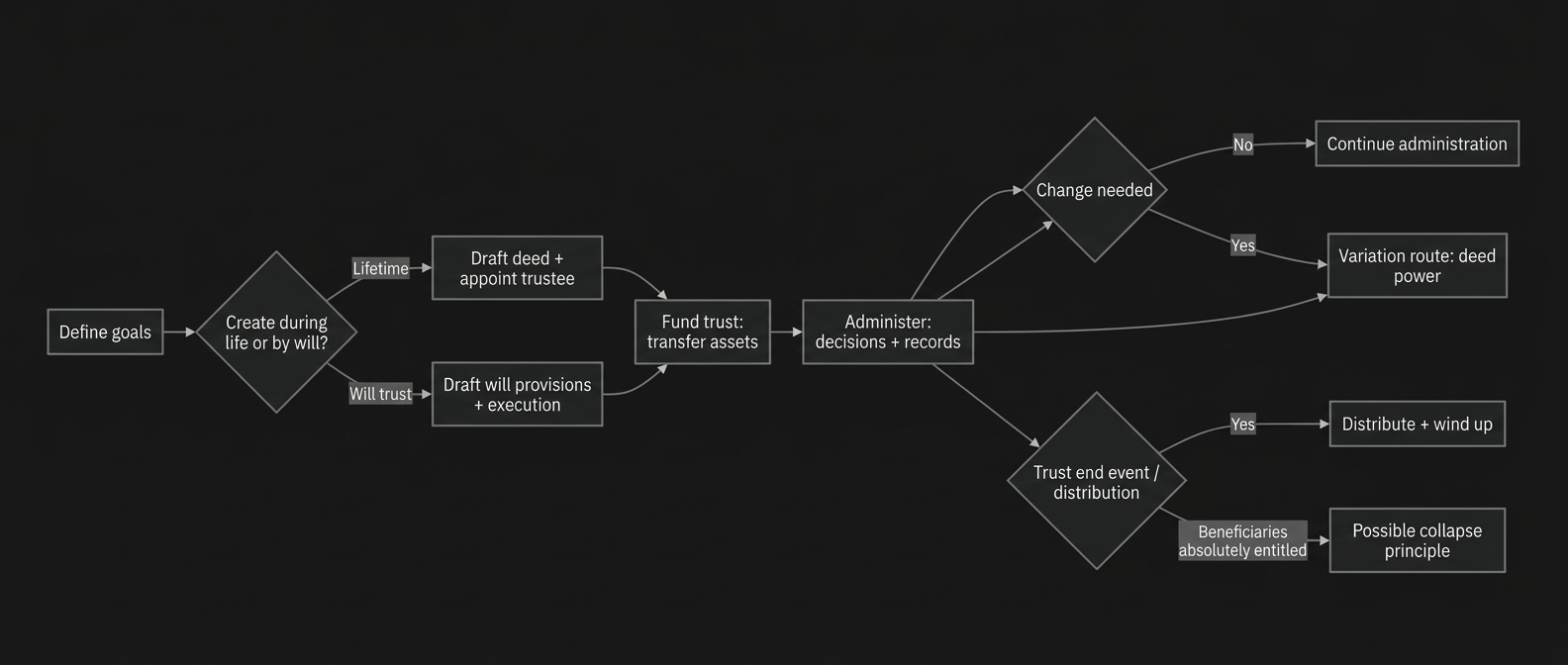

1. The Birth: Creation and Funding

A trust doesn’t exist just because you thought about it. It requires a specific legal “spark.” This usually starts with the Trust Deed (which we covered in detail in our previous article on drafting).

However, the most common mistake people make is thinking that signing the paper is the end of the job. It isn’t. For a trust to actually “live,” it must be funded.

The Transfer of Legal Title

Funding is the process of moving assets from your personal name into the names of the Trustees.

- Property: You must register the change of ownership at the Land Registry.

- Cash: You need to open a specific Trust Bank Account.

- Shares: Share certificates must be re-registered.

If the assets aren’t legally transferred, the trust is “imperfectly constituted.” In plain English? It doesn’t exist yet, and the tax benefits or protections you were hoping for won’t apply.

The Three Certainties

For the trust to be valid from day one, it must satisfy the “Three Certainties”:

- Certainty of Intention: It must be clear you actually meant to create a trust.

- Certainty of Subject Matter: It must be clear exactly what assets are being trusted.

- Certainty of Objects: It must be clear who the beneficiaries are.

2. The Middle Years: Management and Maintenance

Once the trust is funded, it enters its active management phase. This is where the Trustees do the heavy lifting. They have a “fiduciary duty,” which is a fancy legal way of saying they must act in the best interests of the beneficiaries at all times.

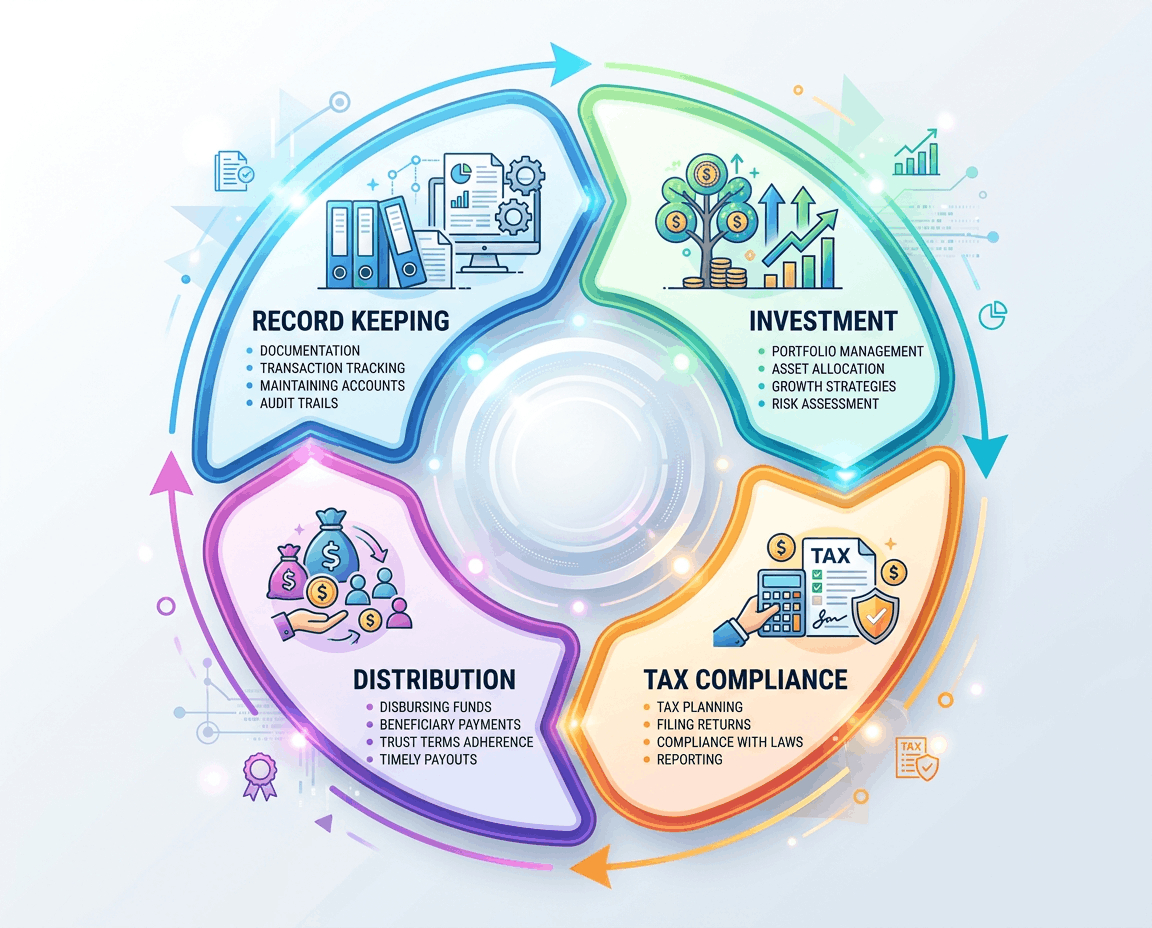

Key Management Tasks

Managing a trust isn’t just about sitting on a pile of money. It involves constant oversight:

| Task | Description | Why it Matters |

|---|---|---|

| Investment | Trustees must invest the trust funds wisely. | To protect the “real value” of the assets against inflation. |

| Tax Returns | Trusts are often separate entities for tax. | Avoiding penalties from HMRC is a top priority. |

| Distributions | Giving money or assets to beneficiaries. | Ensuring the Settlor’s wishes are followed correctly. |

| Record Keeping | Tracking every penny in and out. | Vital if a beneficiary ever questions the management. |

If you’re handling a complex estate, check out our Probate and Estate Administration Guide 2026 for more on how these roles overlap with executor duties.

3. Changing the Rules: The Variation of Trusts Act 1958

Sometimes, life happens. A trust deed written in 1990 might not make sense in 2026. Tax laws change, family members fall out, or the original purpose of the trust becomes impossible to achieve.

Usually, if the trust deed doesn’t give the Trustees the power to change the rules, they are stuck. This is where the Variation of Trusts Act 1958 comes in.

This Act allows the court to “approve” changes to a trust on behalf of beneficiaries who can’t speak for themselves: like children, unborn heirs, or people lacking mental capacity.

Common reasons for Variation:

- Tax Efficiency: Changing the trust structure to avoid new, heavy tax burdens. (See our Inheritance Tax Planning Guide 2026 for context).

- Extending the Life: If a trust is set to end too early, the court might allow it to continue to protect a vulnerable beneficiary.

- Widening Powers: Giving Trustees more freedom to invest in modern assets like digital currency or international property.

While the court has the power to vary a trust, they will only do so if it is for the benefit of those individuals. They won’t let you rewrite the trust just because you don’t like the original Settlor’s vibe.

4. The Beneficiaries Take Control: Saunders v Vautier

What if all the beneficiaries are adults, they all agree, and they simply want the trust to end right now?

There is a famous legal rule called the Saunders v Vautier principle.

Named after a 19th-century court case, this rule says that if all the beneficiaries of a trust are:

- Of “full age” (at least 18 years old);

- Of sound mind (have mental capacity); and

- Are “absolutely entitled” to the trust property…

…then they can collectively tell the Trustees to hand over the assets and close the trust, even if the Trust Deed says they have to wait until they are 30.

Why does this exist?

The law generally believes that if you are an adult and you own something entirely, you should be allowed to do what you want with it. The “dead hand” of the Settlor cannot control the property forever if the living owners decide otherwise.

Visual: A conceptual illustration of “Saunders v Vautier”: a set of keys being handed over, representing the transfer of control from Trustee to Beneficiary.

5. The Sunset: The Conclusion of a Trust

All good things must come to an end. A trust usually concludes in one of three ways:

A. The “Vesting” Date

Most trusts have a natural expiry date written into the deed. This is called the Vesting Date. On this day, the Trustees must distribute all remaining assets to the beneficiaries, and the trust ceases to exist. Under English law, most modern trusts have a maximum lifespan of 125 years (the “Perpetuity Period”).

B. Exhaustion of Assets

Quite simply, if the money runs out because it has all been spent on the beneficiaries (school fees, house deposits, medical care), the trust ends because there is nothing left to manage.

C. The Trustees’ Discretion

In many “Discretionary Trusts,” the Trustees have the power to “appoint” the entire fund to the beneficiaries at any time. Once they distribute the last of the assets, the trust is “wound up.”

Final Steps for Closing a Trust:

When a trust ends, the Trustees can’t just walk away. They must:

- Prepare Final Accounts: Show exactly where the money went.

- Get Indemnities: Ensure the beneficiaries won’t sue them later for honest mistakes.

- HMRC Notification: Formally tell the tax office the trust is closed.

- Distribute Assets: Legally transfer the remaining property or cash.

Why You Need a Pro

Navigating the trust lifecycle: especially the tricky parts like the Variation of Trusts Act 1958 or the Saunders v Vautier rule: requires a steady hand. One wrong move with a tax filing or a distribution can lead to personal liability for the Trustees.

At Judge Law, we’re here to make sure the “middle years” of your trust are smooth and the “sunset” is stress-free. Whether you’re a Trustee looking for guidance or a beneficiary wondering about your rights, we can help you cut through the jargon.

If you’re worried about how your family assets are being managed, or if you need to set up a trust for a specific property purchase, check out our Expert Conveyancing services or reach out to our estate planning team today.

Let’s make sure your legacy follows the right path, from the first signature to the final distribution.