If you’re considering remortgaging your property in Windsor or London, you might be wondering whether you need a solicitor and how the legal process differs from when you first bought your home. The answer isn’t always straightforward, and getting it wrong could cost you time, money, or even put your property at risk.

Let’s break down everything you need to know about remortgage conveyancing, so you can make informed decisions and avoid common pitfalls.

When Do You Actually Need a Conveyancing Solicitor?

The simple rule is this: if you’re switching to a new lender, you’ll need a conveyancing solicitor. Here’s why:

When you change mortgage lenders, your new lender needs to register their legal charge against your property with HM Land Registry. This involves removing your current lender’s charge and replacing it with the new one. Only qualified solicitors or licensed conveyancers can handle this legal work.

However, if you’re staying with your existing lender and simply switching to a different mortgage product (called a “product transfer”), you won’t need any legal work. You can complete this switch within days rather than weeks, and you’ll avoid conveyancing costs entirely.

Additional Situations Requiring Legal Help

You’ll also need a property solicitor if you’re:

- Adding or removing someone from the mortgage (transfer of equity)

- Releasing equity from your property to fund home improvements or other expenses

- Changing from joint to sole ownership or vice versa

- Dealing with leasehold complications that require lease extensions or variations

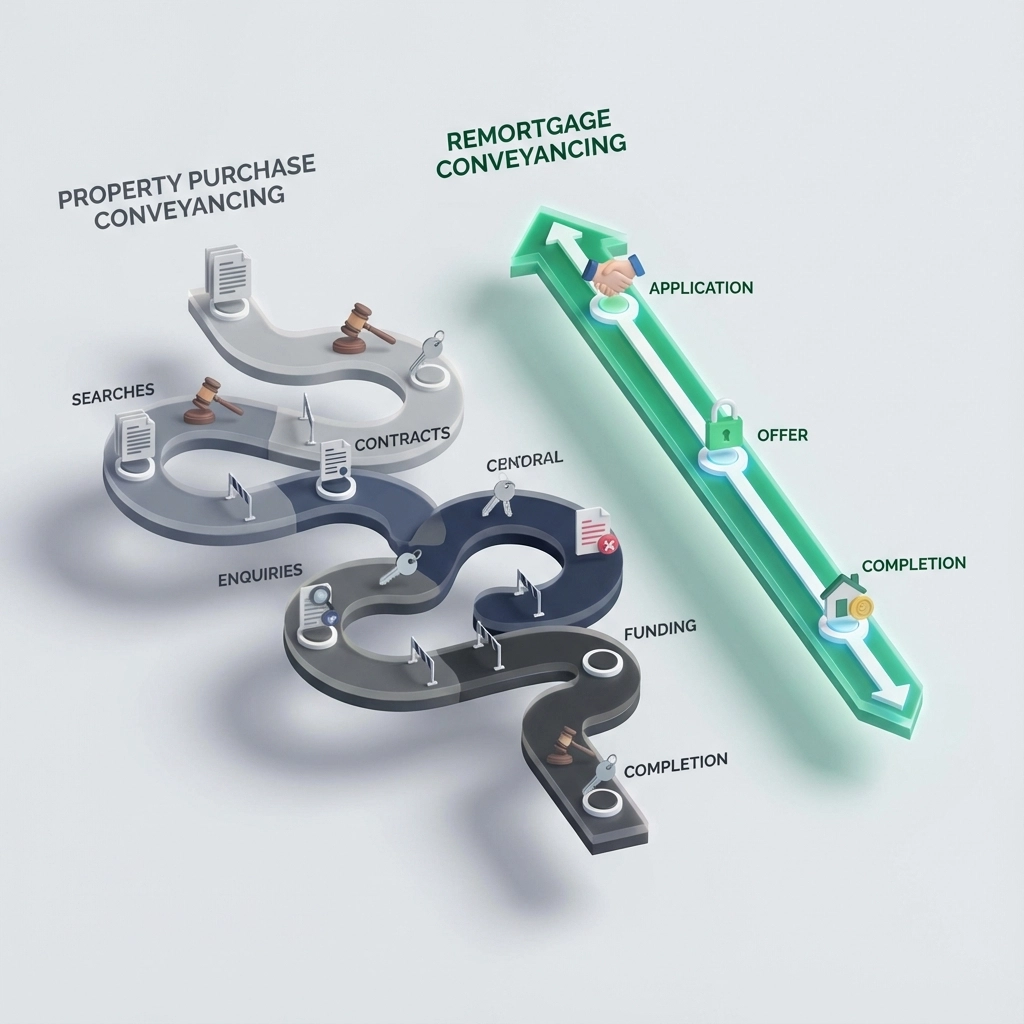

How Remortgage Conveyancing Differs from Buying or Selling Property

The good news is that remortgage conveyancing is typically much quicker and less complex than purchase conveyancing. Here’s how they compare:

Speed and Simplicity

While buying a property can take several months, a standard remortgage with a new lender usually takes 4-8 weeks from application to completion. The process is faster because:

- You already own the property, so there’s no chain to worry about

- Less extensive searches are required

- Your new lender’s requirements are typically less stringent than when you first bought

- There’s no need for extensive property investigations

Reduced Search Requirements

When you first bought your property, your conveyancer likely conducted numerous searches including environmental, water, drainage, and highways searches. For a remortgage, your conveyancer typically only needs:

- A basic local authority search

- Land Registry searches

- Bankruptcy searches against the property owners

Many lenders accept search indemnity insurance instead of fresh searches, which can speed up the process significantly.

The Step-by-Step Remortgage Conveyancing Process

Understanding what happens at each stage can help you prepare and avoid delays:

1. Initial Instructions and Identity Checks

Your conveyancing solicitor will verify your identity through anti-money laundering checks. You’ll typically need to provide:

- Passport or driving licence

- Recent utility bill or council tax bill

- Bank statements

2. Title Investigation

Your conveyancer obtains official copies from Land Registry to confirm:

- You own the property as stated

- Details of your current mortgage

- Any restrictions, covenants, or rights affecting the property

- For leasehold properties, remaining lease term and ground rent details

3. Mortgage Offer Review

Once your new lender issues the formal mortgage offer, your conveyancer reviews all conditions to ensure they can be met. This might include requirements about:

- Property valuation

- Buildings insurance arrangements

- Minimum lease terms (for leasehold properties)

4. Redemption Statement

Your solicitor contacts your current lender to obtain an exact payoff figure, including:

- Outstanding mortgage balance

- Accrued interest to completion date

- Any early repayment charges or exit fees

5. Pre-Completion Searches

Critical searches are conducted close to completion:

- Official Search with Priority: Protects your transaction for 30 working days

- Bankruptcy searches: Confirms no property owners are subject to insolvency proceedings

6. Certificate of Title

Your conveyancer submits a certificate to your new lender confirming everything is acceptable and requesting the mortgage funds.

7. Completion Day

Your solicitor receives the new mortgage funds and uses them to:

- Pay off your existing mortgage in full

- Settle legal fees and disbursements

- Transfer any surplus funds to you (if you’ve borrowed additional money)

8. Post-Completion Registration

Finally, your conveyancer registers the new mortgage at Land Registry, which can take several weeks to complete.

What Your Conveyancer Does to Protect You

Your residential conveyancing solicitor acts as your legal guardian throughout the process, providing crucial protections:

Verifying Title: They ensure you have good legal title and identify any issues that might affect the property’s value or your ability to sell in future.

Checking Restrictions: They review any covenants, easements, or planning restrictions that might limit how you can use your property.

Confirming Insurance: They ensure your buildings insurance meets your new lender’s requirements and provides adequate cover.

Managing Timing: They coordinate with both lenders to ensure the old mortgage is redeemed on the exact day the new one completes, avoiding costly interest charges.

Common Pitfalls to Avoid

Even though remortgage conveyancing is simpler than buying a property, several things can still go wrong:

Leasehold Issues

If you own a leasehold property, your new lender may require:

- At least 80+ years remaining on the lease

- Reasonable ground rent levels

- Proper building insurance arrangements through the management company

Tip: Check your lease terms early in the process. If there are issues, address them before applying for your new mortgage.

Insurance Gaps

Some homeowners cancel their existing buildings insurance too early, leaving a dangerous gap in cover. Your conveyancer will ensure continuous insurance coverage throughout the switch.

Timing Problems

If your current mortgage deal is coming to an end, don’t leave your remortgage too late. Standard variable rates can be significantly higher than your current deal, costing you hundreds of pounds monthly.

Hidden Property Issues

Even for a remortgage, your conveyancer may discover:

- Outstanding planning enforcement notices

- Restrictive covenants you weren’t aware of

- Rights of way affecting your property

- Building regulation issues with previous work

Frequently Asked Questions

Q: Can I use any solicitor for my remortgage?

A: Your new lender will have a panel of approved solicitors and conveyancers. You can choose any firm from this panel, but using a firm that’s not on the panel will slow down your transaction significantly.

Q: How much do conveyancing fees cost for a remortgage?

A: Remortgage conveyancing fees are typically lower than purchase fees, usually ranging from £300-£800 plus disbursements (search fees, Land Registry fees, etc.).

Q: What if I want to borrow additional money against my property?

A: This is called “further advance” or “additional borrowing.” The conveyancing process is similar, but your solicitor will ensure the extra funds are used for acceptable purposes according to your lender’s criteria.

Q: Do I need an environmental search for a remortgage?

A: Usually not. Most lenders accept search indemnity insurance instead of commissioning fresh environmental searches, which speeds up the process.

Q: What happens if problems are discovered during the remortgage process?

A: Your conveyancer will discuss any issues with you and your new lender. Minor problems can often be resolved with indemnity insurance, while major issues might require additional legal work or could affect your mortgage application.

Expert Remortgage Conveyancing in Windsor and London

At Judge Law, our expert residential conveyancing team, led by experienced property solicitor Naresh Suppal, understands the unique challenges facing property owners in Windsor and London. We’ve helped hundreds of homeowners successfully remortgage their properties, avoiding costly delays and protecting their interests throughout the process.

Whether you’re switching lenders to secure a better rate, releasing equity for home improvements, or dealing with complex leasehold issues, our conveyancer team provides the expert guidance you need.

Don’t risk your property transaction by cutting corners on legal advice. Contact our conveyancing solicitors today for a straightforward discussion about your remortgage plans and how we can help protect your interests throughout the process.

Your home is likely your most valuable asset – make sure it’s properly protected with expert legal advice you can trust.