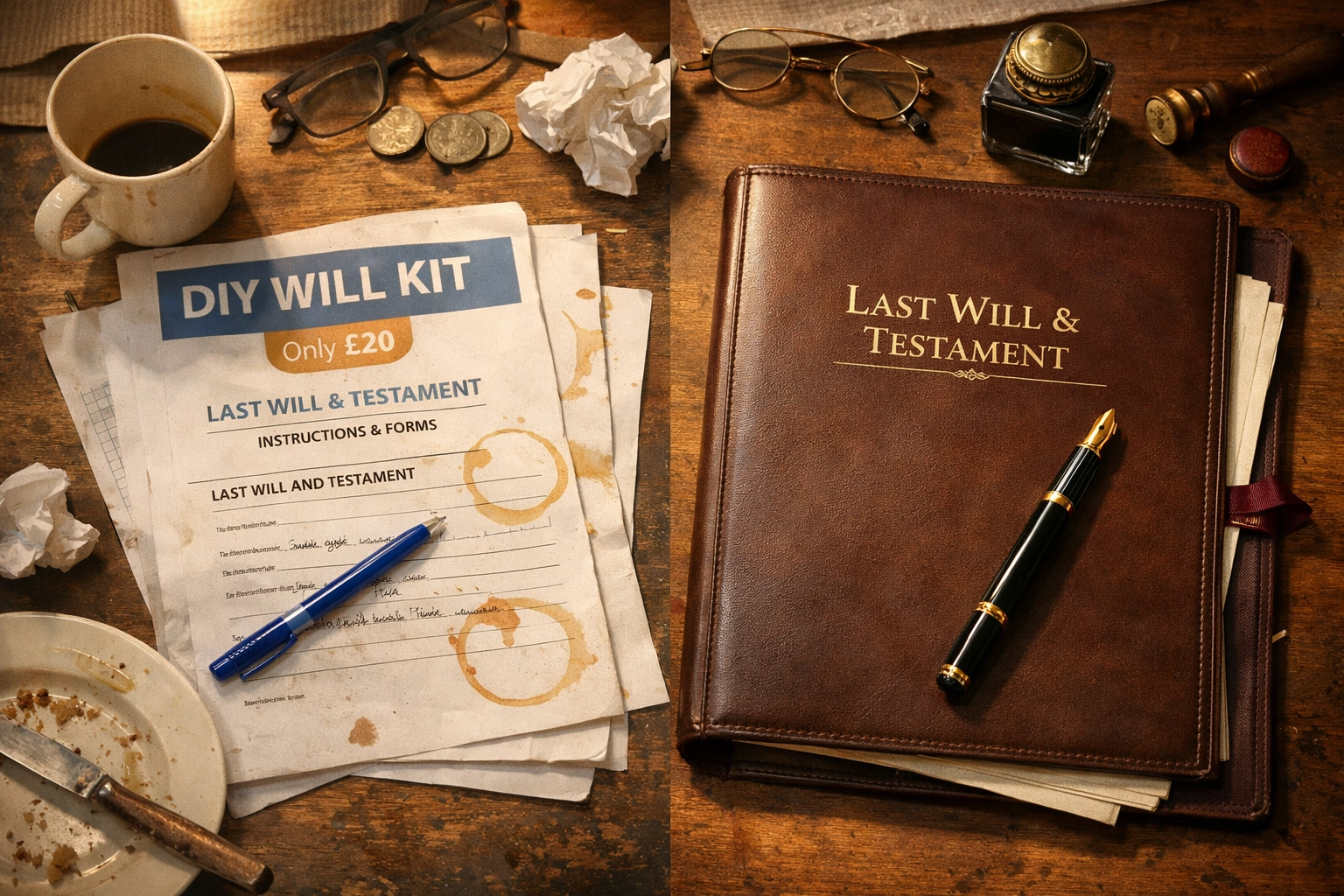

You've probably seen them, those £20 will kits at the post office, or the online templates promising to "sort your estate in 10 minutes." And let's be honest, it's tempting. Why spend £300 on a solicitor when you can knock out a will for the price of a takeaway?

The short answer? Because your family might end up paying thousands, or even losing their inheritance entirely, when that cheap will falls apart.

It's February 2026, and we're seeing more contested estates than ever before. Not because people didn't write wills, but because they wrote the wrong kind of wills. If you've got a blended family, a property, or anything more complicated than "leave everything to my spouse," a DIY will is a gamble you probably can't afford to take.

Let me walk you through what actually happens when a £20 will goes wrong.

The £20 Trap: What You're Actually Buying

DIY will kits typically cost between £10 and £50. Compare that to professional wills solicitors, who charge £150 to £500+ depending on complexity. On paper, it's a no-brainer.

But here's the catch: when you buy a DIY kit, you're also buying all the liability.

Most DIY services, whether it's a paper template or an online form, explicitly exclude any responsibility if your will turns out to be invalid. Read the small print and you'll find phrases like "we accept no liability for errors or omissions."

Professional will writers, on the other hand, carry indemnity insurance. If they make a mistake, there's a compensation scheme to fall back on. With a DIY kit? You're on your own. Or rather, your grieving family is on their own, trying to untangle a legal mess you left behind.

When "Simple" Estates Aren't Simple At All

Most people think their situation is straightforward. "I'll leave everything to my partner. Easy."

Except it's not easy if:

- You're in a second marriage and have children from your first

- You own property jointly (but not as "joint tenants")

- Your partner isn't British and you have cross-border assets

- You have stepchildren you want to provide for

- One of your beneficiaries has a gambling problem or is going through a divorce

These are the situations where DIY wills collapse. You think you've written "leave the house to my wife," but because you didn't specify how she inherits it, she ends up in a dispute with your adult kids over whether it counts as part of the residuary estate.

Or you've written "split everything equally between my three children," but one of them is a stepchild who was never formally adopted, so legally, they have no automatic claim under your will. Cue a costly Inheritance Act claim.

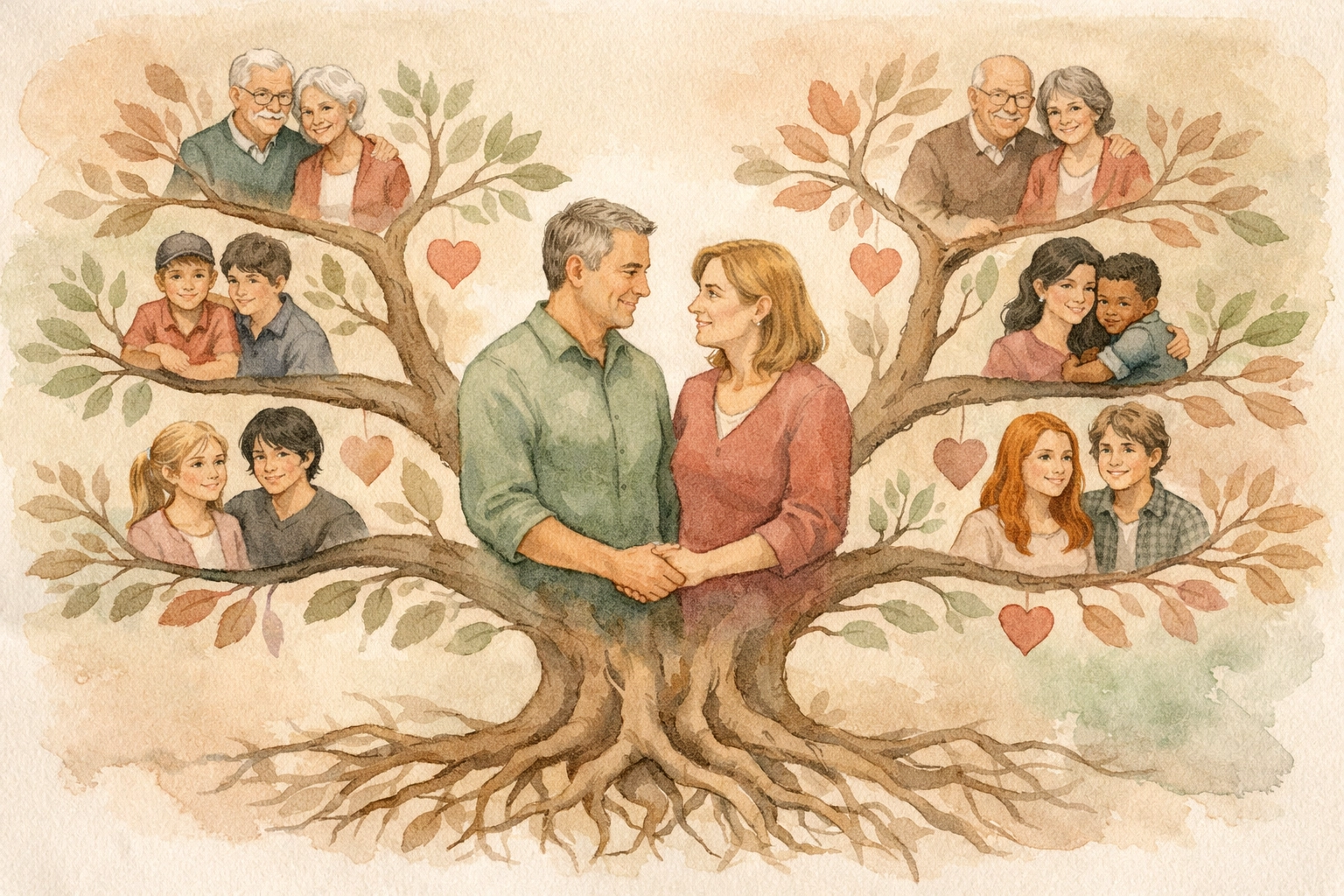

The "Modern Family" Problem

Here's where DIY wills really struggle: they're designed for nuclear families from the 1950s, not the reality of 2026.

Let's say you're on your second marriage. You've got two kids from your first marriage (now in their 20s), and your current partner has a daughter from her previous relationship. You own a house together, and you've got some savings and a pension.

A template will asks: "Who do you want to inherit your estate?"

You write: "My wife, and then my children."

Sounds fair, right? But what actually happens?

Your wife inherits everything when you die. Ten years later, she remarries. When she dies, her new husband inherits her estate, including your money, and his children inherit after him. Your biological children? They get nothing.

This isn't a rare edge case. This is the default outcome for thousands of blended families who use off-the-shelf wills.

The professional alternative? A solicitor would set up a life interest trust, your wife gets to live in the house and use the income, but when she dies, the capital goes to your children, not hers. It's not complicated law. But it's invisible to a DIY kit.

What Actually Goes Wrong: Real Scenarios

Here are the DIY will disasters we've seen in 2026 alone:

1. The Invalid Witness

You need two independent witnesses for your will. Your DIY kit tells you this. What it doesn't tell you is that if one of your witnesses is married to a beneficiary, that beneficiary loses their inheritance.

So when you ask your son-in-law to witness your will, the one leaving your house to your daughter, your daughter's inheritance is void. The house goes through intestacy rules instead, and the family you were trying to protect ends up in a legal battle.

2. The Ambiguous Gift

You write: "I leave my jewellery to my daughters."

Which daughters? The two from your first marriage, or all three including your stepdaughter? And what counts as "jewellery"? Your wedding ring, obviously. But what about your Rolex, or your late mother's brooch that's now worth £15,000?

Ambiguity = litigation. And litigation costs tens of thousands in legal fees.

3. The Missing Executor

You name your brother as executor. He's 68. You die 15 years later, and he's developed dementia. Now your estate is stuck because there's no valid executor, and your family has to apply to the court to appoint someone, a process that takes months and costs thousands.

A proper will includes substitute executors. DIY kits often don't prompt you to think about this.

The Inheritance Tax Time Bomb

Most DIY wills completely ignore inheritance tax planning. If your estate is worth more than £325,000 (or £500,000 if you're passing on your home to direct descendants), your family will pay 40% tax on everything above that threshold.

But here's what professional estate planning solicitors know: there are legal ways to reduce that bill, including:

- Spousal exemptions

- Lifetime gifts (if structured correctly)

- Trusts that protect assets while keeping them available for use

- Business property relief for company shares

None of this shows up in a £20 template. And the cost of getting it wrong? A £200,000 tax bill that could have been £50,000.

When DIY Might Be Okay (But Probably Isn't)

To be fair, there are situations where a DIY will works fine:

- You're single with no kids

- You're leaving everything to one person with no conditions

- You own no property

- You have no savings over £10,000

- You have no complicated family dynamics

If that describes you, then yes, a £20 kit might do the job.

But if you're married, own a home, have children, or have been married before? You're playing with fire.

What Professional Planning Actually Gives You

When you work with a wills solicitor, you're not just paying for a piece of paper. You're paying for:

- A legal audit of your family situation, assets, and wishes

- Tax planning to legitimately reduce your inheritance tax bill

- Future-proofing with substitute executors and guardians for children

- Conflict prevention, wording that's legally watertight, not open to interpretation

- Peace of mind that if something goes wrong, there's professional indemnity insurance to compensate your family

The average cost in 2026? Between £300 and £600 for a straightforward will, or up to £1,500 for more complex estates involving trusts or business assets.

Yes, it's more than £20. But think of it like this: you wouldn't use a £20 online form to buy a house. Why would you use one to distribute everything you've spent your life building?

The Judge Law Approach

At Judge Law, we take wills and estate planning seriously: not because we want to scare you, but because we've seen what happens when families are left to pick up the pieces of a DIY disaster.

We work with clients in Windsor and West London who often have blended families, second homes, or cross-border estates. These aren't unusual situations anymore: they're the norm. And they need more than a photocopied template from 1987.

Our process is straightforward:

- We sit down and actually listen to what you want to achieve

- We map out your assets, your beneficiaries, and any potential conflicts

- We draft a will that's legally sound, tax-efficient, and crystal-clear

- We store it securely and update it when your circumstances change

It's not expensive. It's not complicated. And it might save your family from years of heartache.

The Real Question You Should Be Asking

It's not "Can I afford a solicitor?"

It's "Can my family afford the consequences if I don't use one?"

Because that £20 saving today could cost them £20,000 in legal fees, disputed assets, and unnecessary tax tomorrow.

If you've got anything more complicated than a goldfish and a savings account, it's worth getting it right.